At Integras Partners, we remain focused on the strength of the broader economy, even if cracks begin to develop in the AI narrative. Many underlying economic indicators remain encouraging. Employment is healthy; manufacturing has improved, consumer spending remains resilient, and businesses continue to invest in growth. Corporate profitability is also strong, supported in part by productivity gains that have accelerated in recent years.

There are risks, of course. Market returns have become increasingly concentrated in a relatively small group of companies connected to the AI buildout. That concentration increases the market’s sensitivity to any disruptions in the story. With inflation remaining above the Federal Reserve’s target, the possibility of higher interest rates remains a risk to both the economy and financial markets.

We are also mindful that bull markets do not last forever. This one has been supported by healthy consumer spending, improving business productivity, strong corporate profits, and abundant available cash. These ingredients remain largely intact today; however, markets are already priced high due to a great deal of optimism about the future. If corporate earnings growth slows, productivity gains disappoint, or interest rates move higher, stock prices will face pressure.

This is the challenge investors face today. The economy remains healthy, but much of the stock market’s leadership is increasingly tied to a single theme. Either the benefits from AI arrive quickly enough to support today’s price levels, or markets will adjust.

At Integras Partners, we continuously evaluate these tradeoffs and position client portfolios accordingly. Our primary focus is to ensure that clients can enjoy their lifestyle without worrying that market volatility or today’s headlines will affect tomorrow’s plans. That happens with understanding your goals, building a plan around the life you want to live, and aligning investments to the timelines when those assets will be needed.

The first half of 2026 reminded us that markets tend to focus on what comes next, while headlines focus on what just happened. Investing, instead of speculating, looks beyond the headlines with the objectives of growing wealth without unnecessary risk.

2026 began with high market expectations which are now shaken by renewed conflict in the Middle East, and the resulting higher energy prices and concerns of heightened inflation. As headlines became increasingly dramatic, markets often reacted sharply to new developments. Yet, despite some shaky periods, stock prices have moved higher and the broader economy continued to show resilience.

Today, much of investor optimism is tied to artificial intelligence. The capital being directed toward AI infrastructure, computing power, and implementation is enormous. Supporters believe we are still in the early stages of a multi-year transformation that could meaningfully improve productivity across many industries. If so, the economic benefits could be substantial.

At the same time, markets have become increasingly dependent on that outcome. Investors are betting not only that AI will change the economy, but that those benefits will arrive on a timeline that justifies today’s valuations.

To learn more about Integras Partners’ investing outlook, click below.

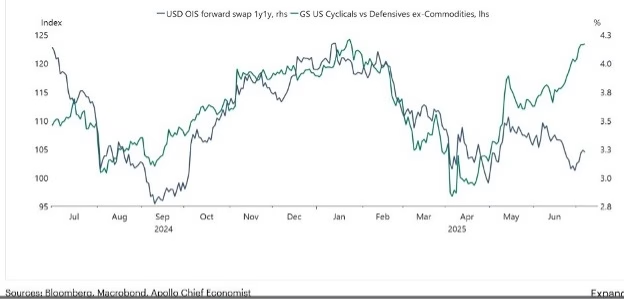

The Fed remains reluctant to lower short-term interest rates, as the inflation outlook heads back up towards 3%. Slowing economic growth and sustained employment weakness would prompt rate cuts.

The technical chart below reflects that the bond market is expecting slower economic growth. Projections are for two interest rate cuts before the end of the year.

Equity markets are signaling the opposite, by valuing cyclical stocks higher than defensive stocks. This happens when the broad market expects an acceleration of economic growth (which leads to higher rates).

Both cannot be right. Either the bond market is wrong and interest rates will move higher, or the stock market is wrong and will see declines. No one knows which it will be. This is the dilemma investors face when positioning their portfolios.

At Integras Partners, we recently increased our more defensive allocations. Markets are shrugging off multiple concerning trends. There are downside risks in a cautious U.S. consumer, slowing economic growth, and weaker employment data not yet reflected in market valuations.

We have concentrated our growth allocations in those sectors less likely to be negatively impacted – sectors where strong secular growth trends remain in place.

It is our nature to err on the side of caution. Chasing returns is not our primary objective. We are motivated every day to ensure that our clients are positioned to enjoy their lifestyle, without worrying about what’s going on short-term in the markets.

If this approach sounds like a good fit for you, please reach out to learn how we can help!

There is an old Wall Street saying that ‘the market goes down in an elevator and rises on an escalator’. The market did indeed fall like an elevator in March but then took the elevator right back up. As tariff postponements soothed markets, stocks staged a major relief rally that continues as of this writing. Simultaneously, the superiority race over artificial intelligence, onshoring production of essential products and increasing operational efficiencies continues unabated across virtually all industries.

After a 19.5% decline which extended through the first week of April, the S&P 500 Index® rebounded a surprising 9.8% during the remainder of the 2nd quarter. The best performance was garnered overseas as the MSCI EAFE Index® finished the quarter up 10.7% and is up 20% YTD. We were glad to see markets finally recognize the cheaper and stronger dividend-paying foreign companies, which we think will continue near-term.

While the détente in the most punitive tariffs sparked the April recovery, the prospect of tariffs has not disappeared. They negatively impact corporate earnings, employment, and inflation. Some companies’ stocks have already been squeezed. The market response to these companies’ quarterly reports will be an interesting indicator of what may manifest later this year.

Future earnings are what matter when valuing a company.

Tariffs will likely remain in place to some degree across most industries, so how companies handle increased costs will sway stock prices.

Economic growth is slowing slightly, and we will closely monitor U.S. consumer strength as data is released over the next months. Anecdotal evidence implies that consumer spending remains strong but is beginning to slow. Employment remains firm as businesses are retaining employees but not hiring many new ones. Strong employment kept us from recession a couple of years ago as consumers had the confidence to continue spending. We don’t expect a major shift, but with today’s elevated stock prices any consumer weakness could cool investor optimism. Unless companies can show earnings growth in a slowing economy, markets will decline. Sectors and industries making major capital expenditures aimed at artificial intelligence and supply chain realignment should be fine, but for others, it will be a challenge.

2025 is a tumultuous year for financial markets, which understandably is rattling even the most experienced investors. While we can’t control investment returns or government policy, focusing on things that you can control may alleviate some of the anxiety.

1. Don’t panic, and remember, this too shall pass. There are scores of historical examples where surges in negative sentiment preceded above-average market returns. In the eight times when sentiment fell by 10% or more in a month, forward returns were higher is seven of them. Average returns 6 months later were +12%, and 12 months later +22%. No one knows that today’s declines will result in a similar experience, but markets usually find a way to rally over walls of worry.

2. Ensure savings accounts are working for you. As you are able, keep some extra cash on hand. Most big bank accounts have pitiful interest rates. Consider a high-yield money market, paying 3.50% or more, and link it to you checking account for ease of moving between accounts when needed.

3. Are your investments actively managed? This is not the best time to be a passive investor, or hold mostly index funds. Continued tariffs will create winners and losers. Market research will be very important to identify vulnerability and opportunity.

The financial markets have been rattled by tariffs. As investors, we reserve judgement on policy and seek to interpret economic impacts on companies we might invest in. We have to assume that tariffs, in some form, will go into effect. A pickup in inflation and lower economic growth is on the table. The impact of this uncertainty is bearish for stocks. The only certainties are that economic and market risk is high, we are in an extremely dynamic situation, and there will be rarely-seen investment opportunities.

As the credit (bond) markets often foretell economic deterioration, when the warnings appeared, we took action. At the end of March, we reduced holdings of more vulnerable sectors in our strategies, like tech and mega-cap stocks. Then when the S&P 500 Index® failed to hold its 200-day moving average (known as a “death cross”), we again took some stock exposure off the table.

Market volatility spikes like this are likely to prove short-lived. When it does settle, we are in position to reinvest parked cash with a constructive long-term perspective. While stocks are random in the short term, they always reward investors over longer periods of time.

Our clients take comfort in knowing that they have truly diversified portfolios. We insulate projected spending for the next few years from market gyrations, so the bulk of investments can remain in stocks for many years to capture gains. So, whether we see a bear market or even an economic recession, our clients are able to continue living life as normal.

Call us today to learn how we can help. 404-941-2800