More and more people are unmarried or living alone by choice. Planning for your future on your own can be empowering yet intimidating at the same time. Many singles greatly value independence, and having a solid plan in place can pave the path to financial independence as well.

Here are a few things to think about as a single-person household:

Build Emergency Savings First: Emergency savings is a foundational piece of any financial plan, but for those living on a single income, an unexpected expense or loss of income could be especially stressful. We recommend using a high yield savings account. The right amount of savings varies for everyone, but a general rule of thumb is 6 months of living expenses.

Invest for Retirement: Planning for retirement becomes even more important when funding it by yourself. If your employer offers a retirement plan with a match, contribute at least enough to capture the full match. Max your contributions if you can, especially in earlier years when your money has the most time to compound. Don’t overlook Roth accounts (if you have access) and taxable accounts. Having the flexibility to withdraw from accounts with differing tax treatment in retirement can stretch your retirement savings further.

Insurance: You probably don’t need life insurance if you don’t have people depending on your income, but consider long-term disability insurance which can replace income If you become disabled. It’s worth evaluating options outside of coverage that your employer may offer – there are differences in benefits, premiums and portability. Also consider long-term care insurance, which can offset costs if you need in-home care or need to move into a care facility later in life. These costs can be great, and it is a mistaken belief that Medicare will cover them.

Estate Planning: Many people think estate planning is only for couples or parents. Without a will or named beneficiaries, the state that you live in will determine what happens to your assets when you die (they will go through a successive list of relatives). You may have more distant relatives, friends, or charities that you wish your assets to go to. It’s also important to think about protecting your wishes when it comes to financial and healthcare decisions, should you become unable to communicate or make decisions yourself. This is where powers of attorney and healthcare directives come into play. If you don’t have a trusted person to act on your behalf, there are options such as attorneys and registered nurse health care advocates.

Integras Partners understands the unique considerations singles face. We help define your goals and create a path to reach them.

Wherever you are on your journey, we’re with you every step of the way.

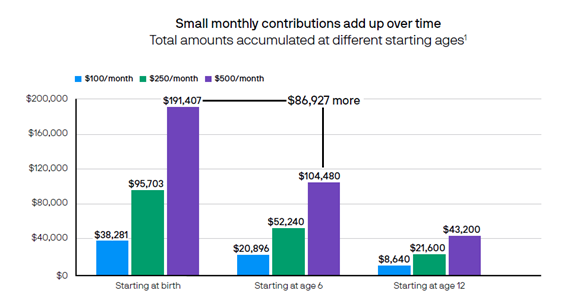

Many families list paying for a child’s college education as an important financial goal, yet are unsure how much to save. College tuition costs have increased much faster in recent decades than any other household expense. J.P. Morgan recently projected that a four-year college education for a child born today will cost between $250k and $580k (ranging from public in-state tuition to private tuition). At the same time, financial aid awards have declined.

If you’re the parent of a newborn, the need for college planning may seem far in the future. But starting early can make a huge difference, even if making small monthly contributions.

A tax-advantaged savings vehicle has the potential to grow faster, as taxes aren’t taking a bite out of your investment returns.

In honor of National 529 Day on May 29th, here we highlight some facts about 529 accounts as a tax-advantaged vehicle for saving and investing for college.

You may get an income-tax break on contributions made to a 529 offered by the state you live in.

Money saved in a 529 has the potential to grow tax-free. Earnings on the money contributed are not taxed while in the 529 account, and money can be withdrawn free from federal income tax if used for qualified educational expenses, including an amount for room and board, and even an annual amount for K-12 education.

Most states also don’t impose state income tax on qualified withdrawals.

Taking money out of a 529 for non-educational expenses triggers tax and penalty only on the gains.

The beneficiary of a 529 account can be changed at any time to another family member or even to yourself. And there is no limit on how long a 529 account can exist – theoretically allowing an account to be passed down generations.

Family and friends can make contributions to your child’s 529, and if a non-parent is the account owner, the money in the 529 plan does not impact federal financial aid.

Subject to certain limitations, up to $35,000 of unused money in a 529 account can be rolled over to a Roth IRA in the beneficiary’s name, without any taxes or penalties related to taking money out for non-educational expenses.

1 J.P. Morgan Asset Management. This hypothetical example illustrates the future values at age 18 of different regular monthly investments for different time periods. Chart also assumes an annual investment return of 6%, compounded monthly. Investment losses could affect the relative tax-deferred investing advantage.

19% of women report feeling confident selecting investments that align with their goals

This is a discouraging statistic from a recent survey conducted on women and investing. We know that a gender gap exists when it comes to investing – on average, data shows that women’s investment account balances are less than men’s. There are a few often-cited reasons for this. The gender pay gap still exists, and women statistically spend more time outside of the workforce, meaning that women may simply have less money to invest.

But there is another reason. Women tend to feel less confident taking investment risk and therefore hold more cash on the sidelines, hampering their money’s growth potential.

But there is a difference between taking risk, and taking inappropriate risk for your goals. Women tend to benchmark successful investing not by the return numbers themselves, but by progress towards goals – buying a house, funding an education, or retiring comfortably.

Defining your goals and their timeframes is the first step toward building the confidence to invest. Money that you don’t need for 10 or 15 years can afford to be invested for growth. The farther along the timeline your goal is, the more certainty you can have of capturing greater returns by investing.

When women do invest, they see results. On average, women outperformed their male counterparts by 40 basis points or 0.4% over a 10-year analysis

On the flip side, studies show that over time, women’s investment returns tend to outperform men’s, with women exhibiting less impulsive investment decisions and staying the course when there is market volatility.

Starting early is the most powerful thing you can do to put yourself on track. If you didn’t start early, start now. Women already have the proclivity to stay invested to meet their goals, we just need the confidence to invest in the first place!

I joined Integras Partners in 2022 wanting to broaden my impact on people’s lives, particularly groups that have been underserved by the financial advice community – groups like women and single earners, which I am also a part of. Integras Partners was already well suited to women investors – focusing on the partnership and the “why” behind financial goals.

I’ll be writing more about these areas in coming newsletters, as well as general financial wellness and investing topics that I hope you will find interesting.

Long-time employees face this non-revocable and permanent choice upon retirement. While the security of lifetime income can be comforting, several trade-offs exist.

Do I want to rely on the company’s future financial strength? How long will I live? What will inflation do to my pension income over time? What happens if I die? Should I take a lower amount to protect my spouse? What happens if they die? Do I have a choice to take a lump sum and control how and when I spend the money?

Pension distributions are limited to lifetime income options without future inflation adjustments. Additionally, If the income beneficiaries die early, there is often no remainder. Many companies offer a “lump-sum distribution” to effectively buy the retiree out of their pension obligation. This amount can be transferred to a traditional IRA tax-free.

There are several advantages to taking the cash.

Freedom to invest the money, timing and adjusting your income, and protecting your heirs. Lump-sum buyouts are calculated using a specified interest rate, so the lump-sum payout value increases in low-rate environments; it increases the lump-sum payout value.

Once you start a pension, you’re locked in. From an IRA, you might take an increased amount until you start Social Security, allowing you to defer and increase your Social Security payment for both you and your spouse. If you have a life event, you can adjust IRA distributions. You cannot adjust a pension. You may downsize your home, get an inheritance, or need to spend a chunk of cash on a new car or family need. A lump sum allows flexibility a pension cannot. Plus, when you die, there is likely an inheritance, which a pension does not offer.

Integras Partners separates lump sum funds into different IRAs, keeping money for short-term needs conservative while allowing assets needed later to grow. Having more time for the remainder to stay invested reduces market risks. Having control of the funds also protects your heirs. Employing good strategies should increase both lifetime income and protect your family.

Most importantly, a “lump-sum rollover” gives you the peace of mind to enjoy what you’ve worked so long to earn truly.

If you’re interested in learning more, give us a call at (404) 941-2800, or reach out to us about your situation.

Required Minimum Distributions (RMDs) take effect the year an IRA owner turns 73, so the government can start collecting taxes. This is payback for making tax-deductible retirement contributions while working. A few years ago, Congress enabled retirees to give any portion of RMDs tax-free charitably!

The Qualified Charitable Distribution option allows for gifting to recognized charities, which counts towards satisfying the RMD. This avoids income tax regardless of whether you are eligible to itemize.

For example, if you typically give $10,000 a year to your favorite charities, you’re probably paying taxes on this money first. So, it costs you $12,200 or more, including taxes. If you make gifts straight from your IRA, you keep more than $2,000 (plus any state tax) in your bank account!

The recipient must be a recognized 501(c)(3) charity (which is typical of religious, education, or community service organizations). Your IRA custodian may have a minimum amount per gift and will have their own paperwork to complete. You can gift as much or to as many charities as you wish, up to the total amount of your RMD.

This is just one of the tax management strategies we employ at Integras Partners. For ideas on how we might help you invest intelligently, nurture your communities, and enjoy financial peace, schedule a call with us!

So, enjoy today and tomorrow, and let us do the worrying!