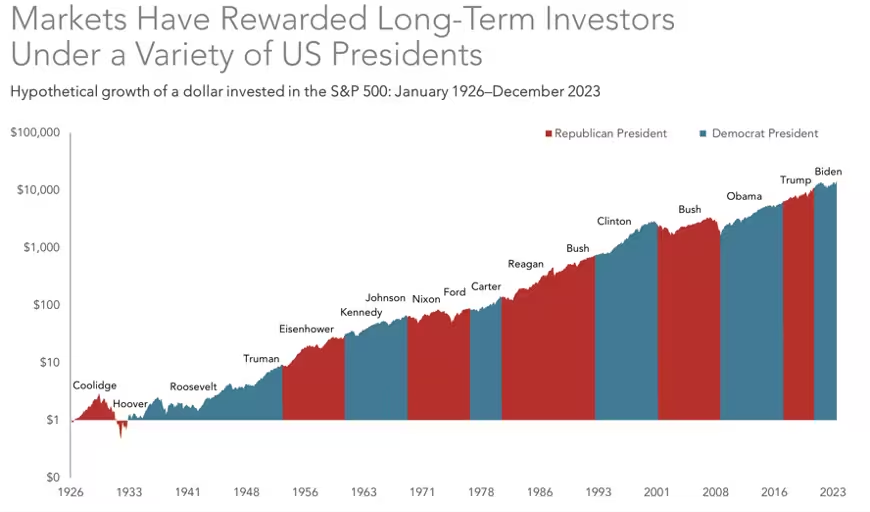

Elections can stir strong emotions, but don’t let them delay your investing. Historically, markets are influenced more by economic fundamentals than politics.

Stock values fluctuate under every president, but the S&P 500 Index® trends higher over the long term, no matter who’s in the Oval Office.

Source: Dimensional Fund Advisors

Or which party controls Congress:

Source: Dimensional Fund Advisors

Market reactions to elections create short-term volatility, but defensive changes to your investments are usually detrimental. Regardless of tax policy or regulations, factors like corporate earnings growth, economic conditions, and technological advancements have more impact on market performance.

Integras Partners with clients to keep a long-term perspective, overcome emotional delays, and take action. By keeping short-term cash needs invested with less market risk, we give clients the peace of mind to keep longer-term money invested and feel more comfortable during periods of short-term market craziness.

Glen & Amber are sandwiched between their elder parents and three children, ages 15-24. Glen has been managing their investments on his own and would like to retire from his corporate job. With family pressures complicating this decision, friends referred them to us for financial advice.

In our Discovery Meeting, we learned that Glen’s parents are in their late seventies and becoming less independent. His sister lives closest to them but increasingly frequent trips are straining her family. Amber’s parents are divorced; her dad and his wife are stable, but her mom is struggling with health and financial issues.

Seeking comfort for Glen’s career decision, we started with the family needs. Through our Generational Conversations program, we provided comprehensive information on care management options. Hiring occasional home caregivers who report to Glen’s sister proved to be a good solution. Amber’s mother moved into independent senior living at a reasonable monthly cost. She is now happier in a social setting and Amber is greatly relieved. The proceeds from selling her mom’s home combined with Social Security will keep mom financially stable for many years.

The couple’s elder daughter, Olivia graduated college with some 529 funds remaining, which we transferred to their middle child. Olivia is now largely independent with a first job, and gets occasional support from her parents.

In addition to increasing 529 contributions for the younger kids, we opened custodial (or UTMA) accounts. These are irrevocable gifts that a parent controls until the children reach their state’s age of majority. Unlike 529’s, they can receive annual gifts of stock and mutual funds and get a preferential tax rate on sales. Glen gifted some appreciated company stock which was promptly sold. The proceeds can immediately cover some extracurricular expenses and later fund college costs ineligible for 529’s like cars, Greek life and entertainment.

With family issues addressed, we narrowed in on the retirement conversation. We explored Social Security strategies. Glen also expects some consulting opportunities. We all agreed to start managing Glen and Amber’s investments right away. Our paradigm of aligning investments to match expected income needs brings comfort around retirement spending, while capturing growth with longer-term dollars.

Generational Conversations also supports adult children and their elder parents to plan for housing, legal strategies and security needs.

Investment performance is not consistent and neither is retiree spending. Early retirees usually travel more and increase spending on hobbies. You may buy a car once every 5 years. Healthcare spending increases as we age. So, why should your portfolio focus on providing a fixed income? Integras Partners adapts portfolio allocations to market dynamics and your changing needs.

We match investments to fulfill projected cash flows. First, we set aside enough money to supplement social security, etc. for up to 30 months depending on our economic outlook. Taking little risk with immediate income provides comfort to spend. The beauty is most of your assets can capture long-term returns without short-term risk.

Integras Partners uses different strategies for graduated time-horizons, optimizing market risk for each timeframe. Every client has unique circumstances and a unique allocation. As a fee-only investment advisor, we don’t charge commissions and are always acting in your best interest.

More and more people are unmarried or living alone by choice. Planning for your future on your own can be empowering yet intimidating at the same time. Many singles greatly value independence, and having a solid plan in place can pave the path to financial independence as well.

Here are a few things to think about as a single-person household:

Build Emergency Savings First: Emergency savings is a foundational piece of any financial plan, but for those living on a single income, an unexpected expense or loss of income could be especially stressful. We recommend using a high yield savings account. The right amount of savings varies for everyone, but a general rule of thumb is 6 months of living expenses.

Invest for Retirement: Planning for retirement becomes even more important when funding it by yourself. If your employer offers a retirement plan with a match, contribute at least enough to capture the full match. Max your contributions if you can, especially in earlier years when your money has the most time to compound. Don’t overlook Roth accounts (if you have access) and taxable accounts. Having the flexibility to withdraw from accounts with differing tax treatment in retirement can stretch your retirement savings further.

Insurance: You probably don’t need life insurance if you don’t have people depending on your income, but consider long-term disability insurance which can replace income If you become disabled. It’s worth evaluating options outside of coverage that your employer may offer – there are differences in benefits, premiums and portability. Also consider long-term care insurance, which can offset costs if you need in-home care or need to move into a care facility later in life. These costs can be great, and it is a mistaken belief that Medicare will cover them.

Estate Planning: Many people think estate planning is only for couples or parents. Without a will or named beneficiaries, the state that you live in will determine what happens to your assets when you die (they will go through a successive list of relatives). You may have more distant relatives, friends, or charities that you wish your assets to go to. It’s also important to think about protecting your wishes when it comes to financial and healthcare decisions, should you become unable to communicate or make decisions yourself. This is where powers of attorney and healthcare directives come into play. If you don’t have a trusted person to act on your behalf, there are options such as attorneys and registered nurse health care advocates.

Integras Partners understands the unique considerations singles face. We help define your goals and create a path to reach them.

Wherever you are on your journey, we’re with you every step of the way.

Ann was facing her next chapter in life. She was recently widowed and had been considering retirement. She wanted to live near grandchildren and downsize her home.

Almost all of Ann’s assets were in a company retirement plan, advised by the plan’s financial advisor. Because they told the advisor that they “didn’t want to lose money”, Ann’s allocation was 55% short-term bonds and 45% cash. She was eligible for a widow’s Social Security benefit but was reluctant to retire, fearful that she didn’t have enough money.

Ann’s fear stemmed from her thinking that she needed to preserve the capital and live off the interest. Our philosophy is that retirees don’t need to preserve all their capital for their heirs, they just need to not run out of money. Ann actually had enough to retire but it was too conservatively invested to meet all of her spending needs throughout retirement. Our layered risk approach allows clients to feel more peace spending in retirement. This is because we take modest risk with investments for the next several years of spending, then capture market returns with the majority of assets that can now remain invested long enough to go through market cycles. This also allows for greater spending over time to account for inflation.

Ann has since moved into her new home and is spending more time with her grandkids. She has the peace of mind to enjoy life knowing that her investments will continue to provide supplemental income with minimal short-term risks.

If you’re interested in discussing how we might help you, please give us a call at (404) 941-2800, or reach out to us here.

Most 401(k) and other retirement plans offer Target Date Funds (TDFs) as a default choice. They have become increasingly popular for a few good reasons but are rarely the best solution once your accounts achieve some size.

Let’s look at how they work and whether they are the most efficient choice for you.

TDFs are a great choice for beginners, or when you join a new employer plan. There is usually a lineup of funds targeting retirement dates in increments of five or so years. The concept is that the fund becomes increasingly conservative as the target date approaches, but that is a one-size-fits-all approach that can’t take your unique needs into account.

So, when are TDFs not the best investment choice?

To start, all of your money is invested with one fund family, instead of getting different approaches and methodologies. These funds are also usually invested across all asset classes and industries instead of those best suited to the current economic environment. They also evenly spread bond exposure instead of actively selecting the most appropriate bond sectors.

The biggest challenge with TDFs is that you don’t want all your investments too conservative as you enter retirement.

Yes, you want to make sure that you have some conservative assets to draw from during rough patches, but you still need growth during retirement to keep pace with inflation.

Here are a few things to consider:

· Do you actively rebalance your accounts?

· Does your plan have tools to evaluate your allocation vs. your goals and timeframes?

· Do you compare what you own against what’s available?

· Have you considered the advantages of an IRA for funds in an old employer plan?

· Are you layering investment risks to match your goal timeframes?