Required Minimum Distributions (RMDs) take effect the year an IRA owner turns 73, so the government can start collecting taxes. This is payback for making tax-deductible retirement contributions while working. A few years ago, Congress enabled retirees to give any portion of RMDs tax-free charitably!

The Qualified Charitable Distribution option allows for gifting to recognized charities, which counts towards satisfying the RMD. This avoids income tax regardless of whether you are eligible to itemize.

For example, if you typically give $10,000 a year to your favorite charities, you’re probably paying taxes on this money first. So, it costs you $12,200 or more, including taxes. If you make gifts straight from your IRA, you keep more than $2,000 (plus any state tax) in your bank account!

The recipient must be a recognized 501(c)(3) charity (which is typical of religious, education, or community service organizations). Your IRA custodian may have a minimum amount per gift and will have their own paperwork to complete. You can gift as much or to as many charities as you wish, up to the total amount of your RMD.

This is just one of the tax management strategies we employ at Integras Partners. For ideas on how we might help you invest intelligently, nurture your communities, and enjoy financial peace, schedule a call with us!

So, enjoy today and tomorrow, and let us do the worrying!

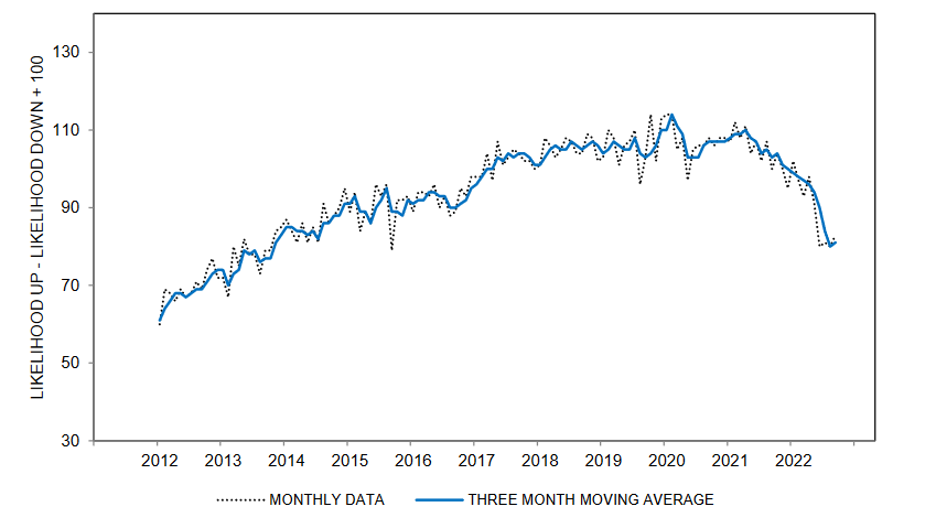

In an ongoing University of Michigan survey, older Americans recently expressed less confidence about having a comfortable retirement.[1]

Inflation is the likely driver of this worry (both inflation itself and the affect it has had on the stock market). To top it off, the inflation that retirees actually experience is typically higher than the headline numbers. This is because retirees spend more on services, such as healthcare and housing, which tend to have a higher inflation rate than goods.

Integras Partners developed investment strategies with retirees in mind. Investment risks needed for growth are limited to longer timeframes. So, money for short-term needs is shielded from market risk. Each client’s unique portfolio allocation is driven by our financial planning process, which accounts for anticipated spending and ongoing inflation.

The big question for investors now is where to be invested going forward. With the overall market trading at 20x earnings and first half gains concentrated into only a select few stocks, most of the market has been left behind. With the valuations of the high-fliers now in excessive territory, the rest of the market looks much more attractive. Value stocks and cyclicals such as financials, energy, materials and consumer staples are a relative bargain and beginning to see some traction. We have maintained value exposure in all of our strategies, seeing better risk/reward near-term than in large growth. Yet the best longer-term risk/reward is in areas not much investor attention has been paid to in several years.

We see potential in sectors and industries left behind in this tech-centric advance. The relative weaker performance of small cap companies to large caps appears to have begun unwinding. We have meaningfully added to small caps in recent months. Today, foreign markets are most attractive as they are generally at lower P/E ratios, and with virtually all regions (except Europe and Japan) growing faster, they offer better value. Plus, when the Fed stops hiking rates, the U.S. Dollar should weaken relative to foreign currencies, which enhances foreign markets’ performance in dollar terms.

We stay focused on what we can control and seek the best longer-term opportunities for growth. The impact and mistakes made during and after the pandemic continue working themselves out. This is a perfect example of the cyclical dangers we work to avoid with our time-appropriate strategies. For our clients with current income needs, we maintain a sufficient level of conservative assets to withstand periods of market weakness until the tide ultimately turns higher. With shorter-term needs funded, longer-term capital can remain invested for growth, and fund future goals. This is part of each client’s personalized investment structure. We like to tell our clients to go live and enjoy life, because we’ve got their backs!

There is a flawed assumption that 4% portfolio distributions are sustainable throughout retirement. Unfortunately, this has proven to be unreliable for too many retirees. The problem doesn’t lie in the math of a withdrawal rate but with the structure of the portfolio.

Retirement portfolios are often assigned a 60/40 allocation (60% stocks with 40% bonds and cash) with monthly distributions drawn proportionately across all assets, regardless of market direction.

In down markets, this strategy forces the sale of more shares to generate cash. The worrisome decision now facing the retiree is whether to increase the pressure on the portfolio by taking the same distributions or to decrease income. Neither is desirable.

Integras Partners takes a healthier approach to retirement income planning.

We layer our clients’ portfolios with designed strategies matching the timeframes of withdrawals.

By isolating more stable assets for short-term spending, we insulate early distributions from random market performance. Assets we don’t need until later have appropriate time to capture growth.

Our clients comfortably spend during market declines without being forced to choose between taking less income or the fear of possibly running out of money.

When faced with a layoff or early retirement, this can be the most difficult decision. We’ve helped hundreds of clients weigh the options, so here are some questions that may be of help to you.

Is my former employer financially stable and is the pension well-funded? When companies have major layoffs, they’re trying to stop bleeding cash. Pensions are rarely completely funded and rely on the continued profitability of the company.

Do I take a reduced benefit to provide for my spouse? Consider your family longevity and personal health habits. If you take the larger amount upfront for the retiree, will you save any of the monthly payments? Women typically live longer and in 25% of couples aged 65, one spouse will live to 95.

How Do I Evaluate the Lump-Sum Option? Many employers offer a Lump-Sum Benefit to “buy-out” their pension obligation. Factors to consider include your personal health status & family longevity, interest rates and inflation, your current situation, the number of years until benefit eligibility, and your feelings about leaving assets to your heirs.

Could I generate more income by investing the money?

Meet Pete and Sandra. They have seen both sons married, purchased their retirement beach home and want to retire soon.

Pete has enjoyed a successful career and built considerable savings and miscellaneous investments to complement his 401(k). They came to us for help to define a sustainable retirement income and professional investment management.

Pete and Sandy elected to work with us because they found comfort in our process, appreciated our Service Model and after firing a brokerage firm, no longer want to make investment decisions. In our first meeting, we discussed how to balance their desire to reduce investment risk while achieving the portfolio growth required for distributions to keep pace with inflation

Integras Analysis

Our answer to this dilemma is our Time Horizon Investment philosophy. We advocate reserving conservative assets for near-term income, which allows longer-term assets to be increasingly oriented to growth. We know that the longer growth investments can stay invested, it becomes more likely for those assets to achieve desirable returns.

Together, we defined anticipated expenses and explored strategies for maximizing Social Security. This enabled us to determine the supplemental cash flows needed from investments. Next, we explored timely investment ideas, long-term care protection and caring for parents. We set a time to share our analysis of current investments, recommendations going forward and visual models of their projected annual situation. We use both comprehensive planning tools and proprietary models to determine how to allocate each client’s resources to our Investment Strategies, providing an increasing income for the first 15 years and ample time for the remainder to pursue long-term growth.

Recommendations

Since Pete is a few years away from retiring there is no need for immediate distributions

Rebalance their investments and established a new account targeted to provide initial income needs and reduce their overall stock exposure

As retirement approaches, migrate to more stable assets to fulfill their earliest income needs

Results

We were able to address their desire to reduce risk, both by educating them on the need to outpace inflation and insulating long-term growth investments with adequate time

They also found value in addressing potential long-term care needs and our Generational Conversation services to facilitate discussing elder parent’s finances, care management, etc.

Our paradigm intentionally avoids the practice of drawing across all investments for income, which can rapidly deplete savings in a down market cycle. For an insightful look at why this is important, review our piece on Why Systematic Distributions are Destined to Fail