Today, U.S. stocks are relatively concentrated. An investor in the S&P 500 is putting 40% of their money in the 10 largest companies. Historically, such concentration doesn’t work out well. The S&P 500 is also expensive. Such a concentrated and expensive market requires corporate earnings to continue growing unabated (to support the prices).

There is rarely economic certainty but until new government policy and the resulting economic impacts are understood, you should expect fairly big market swings. It’s been an unusually long time without a market correction (a 10% decline). One or more market corrections this year would not be surprising, so you should be thoughtful about how your portfolio is invested.

Market corrections can come and go in short order. More protracted declines take longer to develop and recover from. It isn’t so much the loss of value that has the most impact on your portfolio, and your well-being. It is the loss of time. Value will rebuild itself. The question is, do the growth assets in your portfolio have that time?

Integras Partners’ Time Horizon Investment Process can help. You can sustain your lifestyle with the money we set aside in Income Strategies, which provides the time needed for our Growth Strategies to capture the growth rewarded by volatile markets. You’re always welcome to speak with us about how we might guide you. The greatest value we can provide clients is the ability to not worry about money, and to go live life!

Call us today to learn how we can help. 404-941-2800

You’re on your financial journey and we can help people pave their own path. This quarter’s commentary blogs start with a recap of 2024 and our views of economic conditions. Then we share some of our ideas for timely investing. You’re always welcome to speak with us about how we might guide you.

2024 was a year of Artificial Intelligence and the biggest company stocks. Despite December weakness, the S&P 500 Index (a common barometer of the U.S. stock market) gained 25% for the year. However, most of this gain was isolated in the largest and most growth-oriented stocks (most of which are heavy into AI), which investors paid more and more for. Smaller companies showed some strength but faltered as concerns about Inflation prospects and continued economic growth kept coming up. Still, small cap stocks finished the year up 11%. Our robust gains were not shared by the rest of the world. And bonds provided a mild 1.3% return.

Our economy is growing at a healthy rate with low unemployment and inflation around 3%. This supports continued corporate earnings growth and possibly the quite high stock prices we have today. The near future appears primed for further growth as many U.S. consumers are getting raises, have little debt, lots of credit available and job security, all of which encourages more spending. While this all sounds supportive of another good year for markets, you must also consider risks to this view, specifically the relatively high stock prices and how further economic growth impacts inflation and interest rates.

The more an economy grows, the more demand there is for money, which increases long-term interest rates. Also, some policy initiatives voiced by the new administration (i.e. tariffs and deportation) are likely to result in higher costs for US companies. Regulatory reform and a more relaxed tax regime should boost earnings growth. Over the last 3 months, long-term interest rates have risen at almost the fastest pace ever because of these possibilities, and they could potentially go higher. Higher interest rates put downward pressure on stock prices, especially when they are already high.

With stock dividends getting taxed twice (once to the corporation and again to the shareholder), many companies are now choosing to return profits to shareholders in the form of stock buybacks instead. While there are several other reasons, the primary one is this tax-efficiency. Many of these companies do not pay a cash dividend sufficient to be included in our dividend growth strategy today. Integras Partners has historically viewed cash dividends as a sign of corporate strength, but this year we are introducing a new metric to our screening processes that includes these companies in the pool of candidates for investment.

Contact us to learn more about our strategies and how they can help you get where you are going. Call us today to learn how we can help. 404-941-2800

As we age, living situations and health needs will change. Parents and their children avoid planning for them, for very understandable reasons:

Parents don’t “want to be a bother”. Kids “don’t want to pry” into their parents’ lives. Money conversations can be tense. Parents don’t want to choose one child over another to take important roles in making health and financial decisions.

Our Generational ConversationsTM program helps adult children and their elder parents navigate planning for Housing, Care Management, Financial Continuity, Legal Strategies, and Security.

We want to help. As families get together over the holidays, it’s a great time to broach these subjects. Click here to download our free Themes for Family Conversations. We wish you all the joys of the holidays and everyone in your family a little extra peace.

Call us today to learn how we can help. 404-941-2800

Working with Integras Partners brings confidence to your financial journey. We help clients not worry so much about money, knowing that an expert is minding your investments.

Many individual investors let emotions and procrastination impact their decisions – hesitating to buy when prices fall and feeling eager to invest when markets are strong. A disciplined advisor provides steady, informed guidance to improve your financial outcomes.

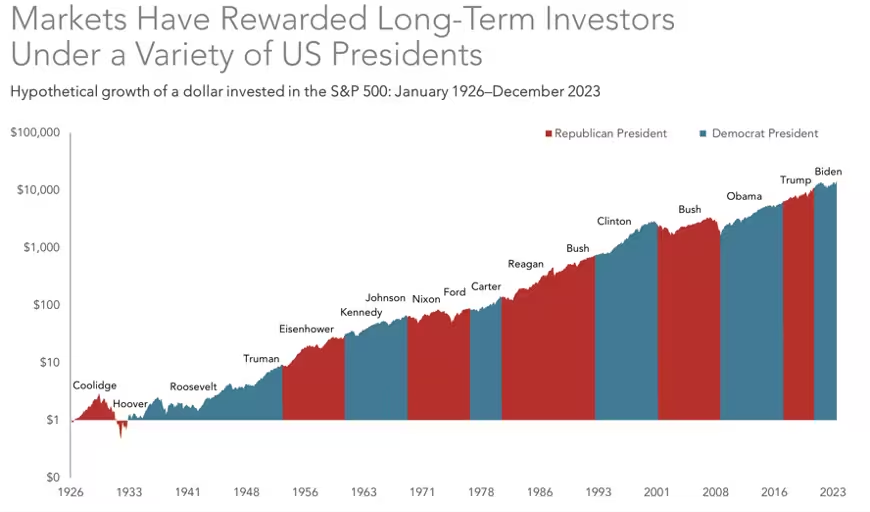

Elections can stir strong emotions, but don’t let them delay your investing. Historically, markets are influenced more by economic fundamentals than politics.

Stock values fluctuate under every president, but the S&P 500 Index® trends higher over the long term, no matter who’s in the Oval Office.

Source: Dimensional Fund Advisors

Or which party controls Congress:

Source: Dimensional Fund Advisors

Market reactions to elections create short-term volatility, but defensive changes to your investments are usually detrimental. Regardless of tax policy or regulations, factors like corporate earnings growth, economic conditions, and technological advancements have more impact on market performance.

Integras Partners with clients to keep a long-term perspective, overcome emotional delays, and take action. By keeping short-term cash needs invested with less market risk, we give clients the peace of mind to keep longer-term money invested and feel more comfortable during periods of short-term market craziness.