As we age, living situations and health needs will change. Parents and their children avoid planning for them, for very understandable reasons:

Parents don’t “want to be a bother”. Kids “don’t want to pry” into their parents’ lives. Money conversations can be tense. Parents don’t want to choose one child over another to take important roles in making health and financial decisions.

Our Generational ConversationsTM program helps adult children and their elder parents navigate planning for Housing, Care Management, Financial Continuity, Legal Strategies, and Security.

We want to help. As families get together over the holidays, it’s a great time to broach these subjects. Click here to download our free Themes for Family Conversations. We wish you all the joys of the holidays and everyone in your family a little extra peace.

Call us today to learn how we can help. 404-941-2800

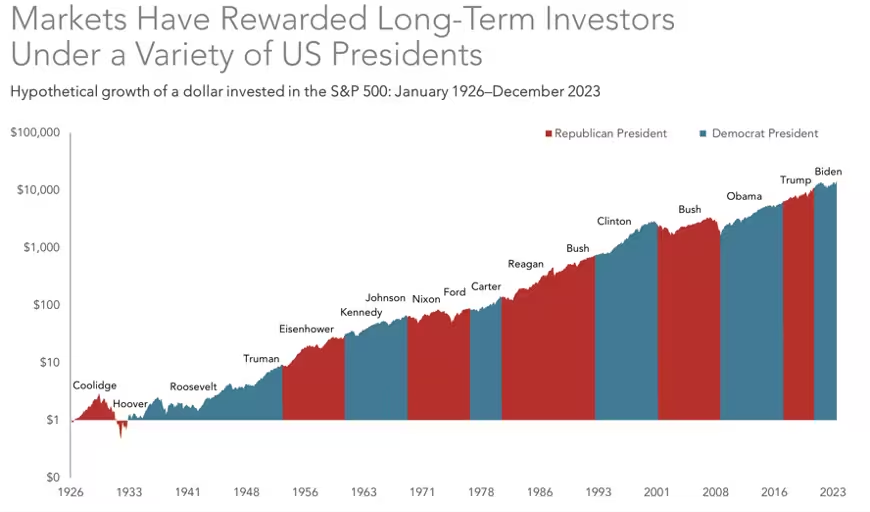

Elections can stir strong emotions, but don’t let them delay your investing. Historically, markets are influenced more by economic fundamentals than politics.

Stock values fluctuate under every president, but the S&P 500 Index® trends higher over the long term, no matter who’s in the Oval Office.

Source: Dimensional Fund Advisors

Or which party controls Congress:

Source: Dimensional Fund Advisors

Market reactions to elections create short-term volatility, but defensive changes to your investments are usually detrimental. Regardless of tax policy or regulations, factors like corporate earnings growth, economic conditions, and technological advancements have more impact on market performance.

Integras Partners with clients to keep a long-term perspective, overcome emotional delays, and take action. By keeping short-term cash needs invested with less market risk, we give clients the peace of mind to keep longer-term money invested and feel more comfortable during periods of short-term market craziness.

First, let’s look at the three types of accounts by their tax treatment.

Tax-Deferred Retirement Accounts are funded with untaxed dollars (contributions are tax deductible, either through salary-deferral or on your tax return). However, future withdrawals are fully taxed as ordinary income. Examples include 401(k)s and traditional IRAs.

Taxable Accounts are funded with after-tax dollars. Dividends and gains from sales receive preferential tax rates. Because you’re paying taxes in the years that income or sales occur, withdrawals aren’t taxed. These are usually mutual fund and stock accounts.

Roth Account contributions are not tax deductible. However, they grow tax-free forever, and withdrawals are never taxed.

It’s best to spread money across these three account types while you are working. This will give you some flexibility to manage your taxes in retirement, which could help your money last longer. Having different types of accounts also provides options for early retirees.

Optimal investment and withdrawal strategies are different for everyone. Factors include age, tax brackets, employer plan features, and investable income. Powerful retirement planning is best done well in advance and then annually while taking distributions.

Retirement planning is one of the most important things that we do for clients. We would be happy to discuss your situation and how we might be of service.

Investment performance is not consistent and neither is retiree spending. Early retirees usually travel more and increase spending on hobbies. You may buy a car once every 5 years. Healthcare spending increases as we age. So, why should your portfolio focus on providing a fixed income? Integras Partners adapts portfolio allocations to market dynamics and your changing needs.

We match investments to fulfill projected cash flows. First, we set aside enough money to supplement social security, etc. for up to 30 months depending on our economic outlook. Taking little risk with immediate income provides comfort to spend. The beauty is most of your assets can capture long-term returns without short-term risk.

Integras Partners uses different strategies for graduated time-horizons, optimizing market risk for each timeframe. Every client has unique circumstances and a unique allocation. As a fee-only investment advisor, we don’t charge commissions and are always acting in your best interest.

More and more people are unmarried or living alone by choice. Planning for your future on your own can be empowering yet intimidating at the same time. Many singles greatly value independence, and having a solid plan in place can pave the path to financial independence as well.

Here are a few things to think about as a single-person household:

Build Emergency Savings First: Emergency savings is a foundational piece of any financial plan, but for those living on a single income, an unexpected expense or loss of income could be especially stressful. We recommend using a high yield savings account. The right amount of savings varies for everyone, but a general rule of thumb is 6 months of living expenses.

Invest for Retirement: Planning for retirement becomes even more important when funding it by yourself. If your employer offers a retirement plan with a match, contribute at least enough to capture the full match. Max your contributions if you can, especially in earlier years when your money has the most time to compound. Don’t overlook Roth accounts (if you have access) and taxable accounts. Having the flexibility to withdraw from accounts with differing tax treatment in retirement can stretch your retirement savings further.

Insurance: You probably don’t need life insurance if you don’t have people depending on your income, but consider long-term disability insurance which can replace income If you become disabled. It’s worth evaluating options outside of coverage that your employer may offer – there are differences in benefits, premiums and portability. Also consider long-term care insurance, which can offset costs if you need in-home care or need to move into a care facility later in life. These costs can be great, and it is a mistaken belief that Medicare will cover them.

Estate Planning: Many people think estate planning is only for couples or parents. Without a will or named beneficiaries, the state that you live in will determine what happens to your assets when you die (they will go through a successive list of relatives). You may have more distant relatives, friends, or charities that you wish your assets to go to. It’s also important to think about protecting your wishes when it comes to financial and healthcare decisions, should you become unable to communicate or make decisions yourself. This is where powers of attorney and healthcare directives come into play. If you don’t have a trusted person to act on your behalf, there are options such as attorneys and registered nurse health care advocates.

Integras Partners understands the unique considerations singles face. We help define your goals and create a path to reach them.

Wherever you are on your journey, we’re with you every step of the way.

Reaching certain ages can be meaningful for financial planning. Age can affect contributions and withdrawal rules from retirement accounts, social security and pension options, and even taxes as many aspects of the tax code are linked to age.

Here are a few significant ages and planning considerations.

50: Eligible to make catch-up contributions to retirement accounts

55: Eligible for penalty exceptions for certain withdrawals from employer retirement accounts

59 ½: Eligible for retirement account withdrawals without early distribution penalty; Potentially eligible to move money from an employer plan to an IRA while still working

60: Beginning in 2025, additional catch-up contributions allowed

62: Earliest age to claim social security (at a reduced benefit amount)

65: Eligible for Medicare coverage (pay attention to enrollment period, which opens prior to 65th birthday); Increase in standard deduction

67: Full retirement age for social security for most people (depends on birth year)

70: Maximum social security benefit is reached

70 ½: Eligible to make Qualified Charitable Distributions

73 or 75: Required minimum distribution age from retirement accounts (depends on birth year)

Integras Partners provides financial planning and investment management to our clients. We have a deep relationship with our clients and understand their needs and goals. The planning process is integral to investment allocation decisions.