The Fed remains reluctant to lower short-term interest rates, as the inflation outlook heads back up towards 3%. Slowing economic growth and sustained employment weakness would prompt rate cuts.

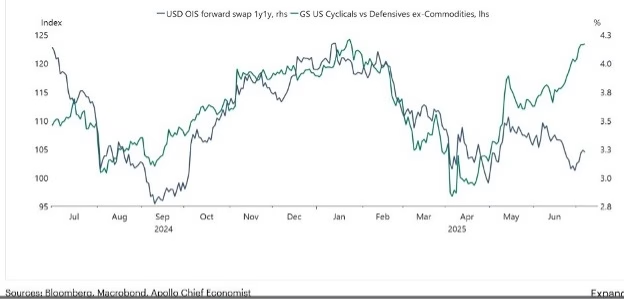

The technical chart below reflects that the bond market is expecting slower economic growth. Projections are for two interest rate cuts before the end of the year.

Equity markets are signaling the opposite, by valuing cyclical stocks higher than defensive stocks. This happens when the broad market expects an acceleration of economic growth (which leads to higher rates).

Both cannot be right. Either the bond market is wrong and interest rates will move higher, or the stock market is wrong and will see declines. No one knows which it will be. This is the dilemma investors face when positioning their portfolios.

At Integras Partners, we recently increased our more defensive allocations. Markets are shrugging off multiple concerning trends. There are downside risks in a cautious U.S. consumer, slowing economic growth, and weaker employment data not yet reflected in market valuations.

We have concentrated our growth allocations in those sectors less likely to be negatively impacted – sectors where strong secular growth trends remain in place.

It is our nature to err on the side of caution. Chasing returns is not our primary objective. We are motivated every day to ensure that our clients are positioned to enjoy their lifestyle, without worrying about what’s going on short-term in the markets.

If this approach sounds like a good fit for you, please reach out to learn how we can help!

There is an old Wall Street saying that ‘the market goes down in an elevator and rises on an escalator’. The market did indeed fall like an elevator in March but then took the elevator right back up. As tariff postponements soothed markets, stocks staged a major relief rally that continues as of this writing. Simultaneously, the superiority race over artificial intelligence, onshoring production of essential products and increasing operational efficiencies continues unabated across virtually all industries.

After a 19.5% decline which extended through the first week of April, the S&P 500 Index® rebounded a surprising 9.8% during the remainder of the 2nd quarter. The best performance was garnered overseas as the MSCI EAFE Index® finished the quarter up 10.7% and is up 20% YTD. We were glad to see markets finally recognize the cheaper and stronger dividend-paying foreign companies, which we think will continue near-term.

While the détente in the most punitive tariffs sparked the April recovery, the prospect of tariffs has not disappeared. They negatively impact corporate earnings, employment, and inflation. Some companies’ stocks have already been squeezed. The market response to these companies’ quarterly reports will be an interesting indicator of what may manifest later this year.

Future earnings are what matter when valuing a company.

Tariffs will likely remain in place to some degree across most industries, so how companies handle increased costs will sway stock prices.

Economic growth is slowing slightly, and we will closely monitor U.S. consumer strength as data is released over the next months. Anecdotal evidence implies that consumer spending remains strong but is beginning to slow. Employment remains firm as businesses are retaining employees but not hiring many new ones. Strong employment kept us from recession a couple of years ago as consumers had the confidence to continue spending. We don’t expect a major shift, but with today’s elevated stock prices any consumer weakness could cool investor optimism. Unless companies can show earnings growth in a slowing economy, markets will decline. Sectors and industries making major capital expenditures aimed at artificial intelligence and supply chain realignment should be fine, but for others, it will be a challenge.

Many people have unanswered questions about setting themselves up for a successful retirement. Below are the primary risks to consider and some general ideas for overcoming them. We help our clients address these risks through financial planning, which starts with identifying the amounts needed to fund goals (like retirement). This conversation is different for everyone, so we invite you to connect.

Underfunding:

Not saving enough for retirement becomes harder to correct in later years. Try to maximize saving through your employer’s retirement plan. Many Americans contribute only the amount that triggers an employer match, failing to adequately fund this primary channel for retirement savings. Since salary-deferral contributions are not taxed, the reduction to your take-home pay is less than any contribution increase.

Overspending:

Be conservative with your portfolio’s growth rate assumption, and try to set your baseline withdrawals below that rate. Overspending early in retirement can be particularly detrimental to the longevity of your portfolio. Consider a flexible withdrawal approach where you can give yourself a “raise” In years when the market performs better than you projected.

Longevity:

Life expectancies are a mid-point, not an end-point. What you don’t want to do is plan to live to age 88 and turn 87 without enough money for the next 10 years. With increasing life expectancy, retirees should plan to spend 35 years in retirement.

Investments too Conservative:

The refrain of maintaining your principal and living off interest is not a good strategy. Inflation compounds every year, so every retiree needs some growth investments to maintain their lifestyle. Growth investments do better over long periods of time and can offset the challenges of increased longevity and rising costs.

Inflation and Medical Costs:

Inflation occasionally spikes (like after COVID), but even a 4% rate doubles your expenses in 18 years. It’s estimated that 80% of your lifetime medical expenses occur in your last five years, and the medical cost inflation rate averages 8%. Be sure to factor rising healthcare and living costs into your retirement planning.

The “4% Rule” is outdated and can compromise a peaceful retirement if markets decline early in your retirement. Integras Partners created time-layered strategies to grow investments with appropriate risk throughout your retirement.

Employer-sponsored retirement plans, like 401(k)s, are designed to encourage saving during your career but are not efficient when it comes time to take money out.

How Withdrawals Are Funded

Many 401(k)s don’t enable choice when investments are sold. Some plans sell pro-rata (every investment is sold based on its percentage of your account). Others use a hierarchy-based approach where investments are sold in a predetermined order, often cash and low-risk assets first, which would leave your remaining investments skewed toward riskier assets. Both methods would mean you’re taking unnecessary risks and leaving investments not aligned to your needs.

Mandatory Tax Withholding

401(k) distributions are typically subject to mandatory 20% federal income tax withholding, regardless of whether this is the right amount for you or how you would like to pay. Effectively, it requires taking an extra 25% of taxable income to realize the same amount of cash.

Required Minimum Distributions (RMDs) and Account Aggregation Rules

Once you reach age 73 (or 75, depending on your birth year), the IRS requires you to take a minimum amount from retirement accounts each year. With 401(k)s, you must calculate and withdraw the RMD from each one separately.

Consider rolling 401(k)s into an IRA for several advantages:

Broader investment choices – 401(k)s typically have a limited menu of investment options which may or may not suit your needs in retirement.

More flexible withdrawal strategies – including the ability to choose exactly which assets to sell and when.

Customizable tax withholding

Ability to aggregate RMDs – If you have multiple IRAs, you can choose to take your combined RMDs from a single account, reducing the likelihood of missing one and incurring a penalty.

If you’re approaching retirement, now is the time to review your options and develop a withdrawal strategy that aligns with your goals, not just your plan’s default settings.

Call us today to learn how we can help. 404-941-2800

Many schools don’t teach Financial Literacy.Beyond a formal education, one of the most powerful gifts you can share is how to manage money.

Encourage them to get started with investing early. Compounding returns over time is like a rolling snowball accumulating more and more wealth.

Does your high schooler or college student have a summer job? Contribute a portion of their earnings to a Roth IRA.

Has your new grad received monetary gifts from family? Talk to them about investing some of that money for their future self.

A single $1,000 investment at age 20 could turn into $80,0001 by age 65. Wait 10 years to make that investment, and it’s less than half the amount by age 65.

First job? Maybe coming up with $1,000 all at once sounds like a lot. What if they could invest just $100 a month?

Investing just $100 a month beginning at age 25 could grow to $530,0001 at age 65! Putting in $48,000 over 40 years and ending up with over $500,000 is pretty compelling.

Treat investing like a bill you pay to your future self. Automate it and let compound growth make life-changing decisions possible.

Here are some ideas to free up money for investing each month.

Cancel subscriptions not used regularly

Make coffee at home

Cook some meals at home

Use cashback credit cards (as long as they’re paid off each month) and invest the bonuses

One last question your kids may have – what if they can’t invest consistently for 40 years? Is it still worth it?

Investing $100 a month beginning at age 25, then stopping at age 45 could still turn into $330,000 by age 651.

The takeaway? Start early and be consistent. Small, regular contributions now can lead to life-changing outcomes later.

Call us today to learn how we can help. 404-941-2800