Investment performance is not consistent and neither is retiree spending. Early retirees usually travel more and increase spending on hobbies. You may buy a car once every 5 years. Healthcare spending increases as we age. So, why should your portfolio focus on providing a fixed income? Integras Partners adapts portfolio allocations to market dynamics and your changing needs.

We match investments to fulfill projected cash flows. First, we set aside enough money to supplement social security, etc. for up to 30 months depending on our economic outlook. Taking little risk with immediate income provides comfort to spend. The beauty is most of your assets can capture long-term returns without short-term risk.

Integras Partners uses different strategies for graduated time-horizons, optimizing market risk for each timeframe. Every client has unique circumstances and a unique allocation. As a fee-only investment advisor, we don’t charge commissions and are always acting in your best interest.

More and more people are unmarried or living alone by choice. Planning for your future on your own can be empowering yet intimidating at the same time. Many singles greatly value independence, and having a solid plan in place can pave the path to financial independence as well.

Here are a few things to think about as a single-person household:

Build Emergency Savings First: Emergency savings is a foundational piece of any financial plan, but for those living on a single income, an unexpected expense or loss of income could be especially stressful. We recommend using a high yield savings account. The right amount of savings varies for everyone, but a general rule of thumb is 6 months of living expenses.

Invest for Retirement: Planning for retirement becomes even more important when funding it by yourself. If your employer offers a retirement plan with a match, contribute at least enough to capture the full match. Max your contributions if you can, especially in earlier years when your money has the most time to compound. Don’t overlook Roth accounts (if you have access) and taxable accounts. Having the flexibility to withdraw from accounts with differing tax treatment in retirement can stretch your retirement savings further.

Insurance: You probably don’t need life insurance if you don’t have people depending on your income, but consider long-term disability insurance which can replace income If you become disabled. It’s worth evaluating options outside of coverage that your employer may offer – there are differences in benefits, premiums and portability. Also consider long-term care insurance, which can offset costs if you need in-home care or need to move into a care facility later in life. These costs can be great, and it is a mistaken belief that Medicare will cover them.

Estate Planning: Many people think estate planning is only for couples or parents. Without a will or named beneficiaries, the state that you live in will determine what happens to your assets when you die (they will go through a successive list of relatives). You may have more distant relatives, friends, or charities that you wish your assets to go to. It’s also important to think about protecting your wishes when it comes to financial and healthcare decisions, should you become unable to communicate or make decisions yourself. This is where powers of attorney and healthcare directives come into play. If you don’t have a trusted person to act on your behalf, there are options such as attorneys and registered nurse health care advocates.

Integras Partners understands the unique considerations singles face. We help define your goals and create a path to reach them.

Wherever you are on your journey, we’re with you every step of the way.

Ann was facing her next chapter in life. She was recently widowed and had been considering retirement. She wanted to live near grandchildren and downsize her home.

Almost all of Ann’s assets were in a company retirement plan, advised by the plan’s financial advisor. Because they told the advisor that they “didn’t want to lose money”, Ann’s allocation was 55% short-term bonds and 45% cash. She was eligible for a widow’s Social Security benefit but was reluctant to retire, fearful that she didn’t have enough money.

Ann’s fear stemmed from her thinking that she needed to preserve the capital and live off the interest. Our philosophy is that retirees don’t need to preserve all their capital for their heirs, they just need to not run out of money. Ann actually had enough to retire but it was too conservatively invested to meet all of her spending needs throughout retirement. Our layered risk approach allows clients to feel more peace spending in retirement. This is because we take modest risk with investments for the next several years of spending, then capture market returns with the majority of assets that can now remain invested long enough to go through market cycles. This also allows for greater spending over time to account for inflation.

Ann has since moved into her new home and is spending more time with her grandkids. She has the peace of mind to enjoy life knowing that her investments will continue to provide supplemental income with minimal short-term risks.

If you’re interested in discussing how we might help you, please give us a call at (404) 941-2800, or reach out to us here.

The S&P 500 Index® gained 15% in the first half of 2024. However, this gain was not as healthy as it appeared on the surface. The top 10 stocks represent more of the S&P than they have at any time in the last 25 years. Without the top 10 stocks, the remaining 490 names were up only 4%. We’ve written about performance disparities in several of our quarterly commentaries – large vs. small companies, growth vs. value, domestic vs. international. These types of disparities can’t last forever – either the rest of the market catches up or the top of the market cools down. We were happy to see some of the former this month, but we still find ourselves in a very concentrated market.

Many newer investors begin with index funds, such as those tracking the S&P 500. The S&P 500 is market-cap weighted, which means the largest companies in the index determine most of its performance. Today, the stock prices of these largest companies tend to move together – they are driven by similar factors such as enthusiasm over AI. So, a decline in one big name often drags the others down. Younger investors should think about broadening their investments (beyond the largest U.S. companies) to gain exposure to additional factors that tend to reward investors over time. Career Builders have the power of time on their side. Investing early in your career is always a good idea.

In addition to the issue of market concentration, there are beginning signs of a cooling economy. We can’t say that a recession is around the corner. U.S. economic growth continues, inflation is crawling lower, and consumer spending on services (travel, etc.) is strong. However, unemployment claims are rising. Broad consumer spending and housing sales are both slowing. Disinflationary forces are beginning to be felt and the earnings growth needed to support stock prices could become challenged. We advise Established Professionals to keep safer investments for money needed in the shorter term. But it is important to keep a long-term perspective for your retirement savings. Fear of the short-term and the emotional investment responses it can cause can be a major detriment to meeting your goal.

In a market trading at 24x earnings, some healthy caution is in order, but we’re not reducing stock exposure at this point. Despite the market’s concentration risks, overall corporate earnings should strengthen the remainder of this year and beyond. Over long periods, markets trend higher, even with downturns and corrections along the way. Our portfolios are structured to withstand these downturns, with money needed in earlier retirement years invested most conservatively.

There is still the question of how long interest rates will remain elevated. We expect to see inflation moderate, and the Fed lowering interest rates as early as September. This should allow capital-intensive businesses and commercial real estate borrowers to refinance at lower rates – feeding economic activity and supporting those smaller-cap stocks that have underperformed the largest companies.

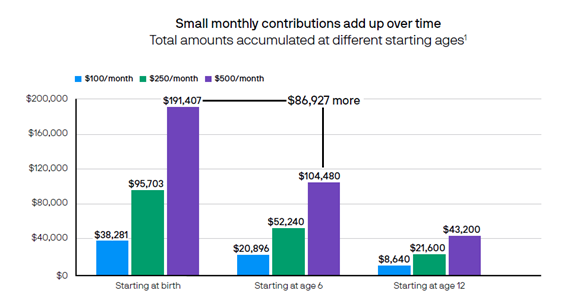

Many families list paying for a child’s college education as an important financial goal, yet are unsure how much to save. College tuition costs have increased much faster in recent decades than any other household expense. J.P. Morgan recently projected that a four-year college education for a child born today will cost between $250k and $580k (ranging from public in-state tuition to private tuition). At the same time, financial aid awards have declined.

If you’re the parent of a newborn, the need for college planning may seem far in the future. But starting early can make a huge difference, even if making small monthly contributions.

A tax-advantaged savings vehicle has the potential to grow faster, as taxes aren’t taking a bite out of your investment returns.

In honor of National 529 Day on May 29th, here we highlight some facts about 529 accounts as a tax-advantaged vehicle for saving and investing for college.

You may get an income-tax break on contributions made to a 529 offered by the state you live in.

Money saved in a 529 has the potential to grow tax-free. Earnings on the money contributed are not taxed while in the 529 account, and money can be withdrawn free from federal income tax if used for qualified educational expenses, including an amount for room and board, and even an annual amount for K-12 education.

Most states also don’t impose state income tax on qualified withdrawals.

Taking money out of a 529 for non-educational expenses triggers tax and penalty only on the gains.

The beneficiary of a 529 account can be changed at any time to another family member or even to yourself. And there is no limit on how long a 529 account can exist – theoretically allowing an account to be passed down generations.

Family and friends can make contributions to your child’s 529, and if a non-parent is the account owner, the money in the 529 plan does not impact federal financial aid.

Subject to certain limitations, up to $35,000 of unused money in a 529 account can be rolled over to a Roth IRA in the beneficiary’s name, without any taxes or penalties related to taking money out for non-educational expenses.

1 J.P. Morgan Asset Management. This hypothetical example illustrates the future values at age 18 of different regular monthly investments for different time periods. Chart also assumes an annual investment return of 6%, compounded monthly. Investment losses could affect the relative tax-deferred investing advantage.

Most 401(k) and other retirement plans offer Target Date Funds (TDFs) as a default choice. They have become increasingly popular for a few good reasons but are rarely the best solution once your accounts achieve some size.

Let’s look at how they work and whether they are the most efficient choice for you.

TDFs are a great choice for beginners, or when you join a new employer plan. There is usually a lineup of funds targeting retirement dates in increments of five or so years. The concept is that the fund becomes increasingly conservative as the target date approaches, but that is a one-size-fits-all approach that can’t take your unique needs into account.

So, when are TDFs not the best investment choice?

To start, all of your money is invested with one fund family, instead of getting different approaches and methodologies. These funds are also usually invested across all asset classes and industries instead of those best suited to the current economic environment. They also evenly spread bond exposure instead of actively selecting the most appropriate bond sectors.

The biggest challenge with TDFs is that you don’t want all your investments too conservative as you enter retirement.

Yes, you want to make sure that you have some conservative assets to draw from during rough patches, but you still need growth during retirement to keep pace with inflation.

Here are a few things to consider:

· Do you actively rebalance your accounts?

· Does your plan have tools to evaluate your allocation vs. your goals and timeframes?

· Do you compare what you own against what’s available?

· Have you considered the advantages of an IRA for funds in an old employer plan?

· Are you layering investment risks to match your goal timeframes?

Reaching certain ages can be meaningful for financial planning. Age can affect contributions and withdrawal rules from retirement accounts, social security and pension options, and even taxes as many aspects of the tax code are linked to age.

Here are a few significant ages and planning considerations.

50: Eligible to make catch-up contributions to retirement accounts

55: Eligible for penalty exceptions for certain withdrawals from employer retirement accounts

59 ½: Eligible for retirement account withdrawals without early distribution penalty; Potentially eligible to move money from an employer plan to an IRA while still working

60: Beginning in 2025, additional catch-up contributions allowed

62: Earliest age to claim social security (at a reduced benefit amount)

65: Eligible for Medicare coverage (pay attention to enrollment period, which opens prior to 65th birthday); Increase in standard deduction

67: Full retirement age for social security for most people (depends on birth year)

70: Maximum social security benefit is reached

70 ½: Eligible to make Qualified Charitable Distributions

73 or 75: Required minimum distribution age from retirement accounts (depends on birth year)

Integras Partners provides financial planning and investment management to our clients. We have a deep relationship with our clients and understand their needs and goals. The planning process is integral to investment allocation decisions.

Changes to the FAFSA form and the formula for determining a family’s need for aid are changing, effective for the 2024-2025 school year. While all the changes are beyond the scope of this post, here we highlight two from a financial planning perspective.

Parent Income:

Contributions (pre-tax salary deferrals) to employer retirement accounts are no longer added back to parent income. This could be an additional incentive for parents with employer plans to max out contributions in years that the FAFSA looks at income. The FAFSA looks at the year two years prior to the beginning of the school year. For example, the 2024-2025 school year looks at 2022 income. Note that this change only applies to contributions that come straight from a salary reduction. Contributions to IRAs that are deductible on the tax return are still added back to parent income.

Grandparent Contributions: Up until now, while grandparent (or other non-parent) owned 529 accounts did not count towards a parent or student’s assets, withdrawals from said account counted as income to the student which had to be reported on the FAFSA. This could reduce the student’s aid eligibility. With the changes, withdrawals from a third-party owned 529 account will no longer count as student income. Grandparents can now maintain a 529 account for their grandchildren and distribute funds without impacting aid eligibility.

Because of these changes, the 2024-2025 form will not be available until December this year. You can stay up to date on announcements at https://studentaid.gov/, or through college financial aid office websites.

Call us to review your investment approach (404) 941-2800.

This inflation cycle has played out much differently than past cycles.

The primary challenge in tackling stubborn inflation today is that the ultra-low rates of the past several years allowed companies to assume long-term debt very cheaply. The Fed’s Open Market Committee (FOMC) can only change the shortest-term interest rates, primarily impacting revolving and floating debt like credit cards and bank loans. The anticipated increase in corporate demand for financing at higher rates never materialized and delinquencies have been well-managed. So, the financial system has remained resilient and provided consumers with the confidence needed to continue spending.

Entering this cycle, consumers were also flush with spending power due to government stimulus, low fixed-rate mortgages, and lower-than-average debt service costs. So, Fed rate hikes haven’t impacted consumer behavior as much as in past cycles. Equally important, companies took advantage of robust demand by raising prices – further feeding inflation – and allowing them to protect or even increase profit margins while retaining their workforce. This self-reinforcing loop has allowed the economy to avoid recession and the stock market to recover faster than virtually every economic indicator – and our own fears – otherwise suggested.

Today we are in a momentum-led rally with the market assuming interest rate cuts later this year and a renaissance of capital spending on Artificial Intelligence over the next many years.

Momentum can carry a market a long way and we have enjoyed a period of market stability without suffering any meaningful pullback. This is rather surprising with 3 of the “Magnificent 7” having underperformed YTD, the Fed lowering projected rate cuts by half, and the past two months of inflation coming in higher than projected. The stock market has defied all but the rosiest of scenarios, with equity issuance (including IPO’s) at the highest level since 2021. This too shall change, but when it does it shouldn’t derail the bull market we are in. Volatility will return to test the conviction of investors. There will be some rougher sledding for us all at some point (it could be sooner rather than later).

Integras Partners strategies allow our clients’ stock exposure to be insulated by time. We don’t take meaningful market risk with money that our clients need soon. We don’t want them to change their spending decisions due to financial markets. Our objective has always been for our clients to enjoy life and leave the worrying to us.

2024 started with concern over stock prices, focused on the widening gulf between the price moves of the “Magnificent Seven” tech stocks and the rest of the market. Expectations for this gulf to close were rooted in the Fed’s actions – when they would begin cutting interest rates and how many cuts would occur in 2024.

At the end of 2023, the bond market had priced in nearly a 100% chance that rate cuts would begin in March.

Our expectation has been that cuts were not likely to begin until this summer. Given the most recent inflation data, and conceivably similar readings to come, it would now not be surprising to see no cuts until even deeper into the year, if at all.

The 1st quarter saw the S&P 500 rally 10% while almost totally discounting Fed rate cuts this year. This could be the market seeing lower rates and slowing inflation ahead, however, inflation is proving to be more difficult to tame towards the Fed’s 2% target. Sticky inflation may prove to be the Achilles heel of the current advance.

We also wrote in our Q4 2023 commentary that the focus of the market would soon turn from interest rates to the market fundamentals of earnings and valuation. This has started coming to fruition, but complicating this calculus is the momentum of any company involved with artificial intelligence, and market expectations for revenues and earnings of all companies due to AI’s influence. While in early days, “AI” has overtaken the narrative of the Fed needing to lower interest rates, and the speculative nature of investors has re-emerged. Today we are in a momentum-led rally with the market assuming rate cuts later this year and a renaissance of capital spending on AI over the next many years.

While the advance has its roots firmly embedded in the AI excitement, other green shoots are becoming visible as well.

Valuations are very attractive in small caps and international stocks, and mutual fund flows are reflecting an increased appetite for value vs. momentum. These are signs of a healthy market – ones that should be embraced, although they will likely be tested.

While not our base case, there is a chance that with financial conditions having eased so much already, a renewed upswing in inflationary forces are taking root. Should the economy remain strong, coupled with government stimulus funds (JOBS Act, Infrastructure, Inflation Reduction Act, etc.) flowing into the economy and consumers continuing to spend, inflation may not recede to the Fed’s 2% goal. Perhaps worse, the Fed may start easing only to have to pivot and raise rates again. These are risks we are mindful of and recognize that regardless of how rosy a set of projections may look now, there are several catalysts that could change investor sentiment in a meaningful way.

We continue monitoring all these factors, watching developments, and adjusting our strategies and client portfolios as necessary. Where there is disruption and change, there is often opportunity.