First, let’s look at the three types of accounts by their tax treatment.

Tax-Deferred Retirement Accounts are funded with untaxed dollars (contributions are tax deductible, either through salary-deferral or on your tax return). However, future withdrawals are fully taxed as ordinary income. Examples include 401(k)s and traditional IRAs.

Taxable Accounts are funded with after-tax dollars. Dividends and gains from sales receive preferential tax rates. Because you’re paying taxes in the years that income or sales occur, withdrawals aren’t taxed. These are usually mutual fund and stock accounts.

Roth Account contributions are not tax deductible. However, they grow tax-free forever, and withdrawals are never taxed.

It’s best to spread money across these three account types while you are working. This will give you some flexibility to manage your taxes in retirement, which could help your money last longer. Having different types of accounts also provides options for early retirees.

Optimal investment and withdrawal strategies are different for everyone. Factors include age, tax brackets, employer plan features, and investable income. Powerful retirement planning is best done well in advance and then annually while taking distributions.

Retirement planning is one of the most important things that we do for clients. We would be happy to discuss your situation and how we might be of service.

The S&P 500 Index® gained 15% in the first half of 2024. However, this gain was not as healthy as it appeared on the surface. The top 10 stocks represent more of the S&P than they have at any time in the last 25 years. Without the top 10 stocks, the remaining 490 names were up only 4%. We’ve written about performance disparities in several of our quarterly commentaries – large vs. small companies, growth vs. value, domestic vs. international. These types of disparities can’t last forever – either the rest of the market catches up or the top of the market cools down. We were happy to see some of the former this month, but we still find ourselves in a very concentrated market.

Many newer investors begin with index funds, such as those tracking the S&P 500. The S&P 500 is market-cap weighted, which means the largest companies in the index determine most of its performance. Today, the stock prices of these largest companies tend to move together – they are driven by similar factors such as enthusiasm over AI. So, a decline in one big name often drags the others down. Younger investors should think about broadening their investments (beyond the largest U.S. companies) to gain exposure to additional factors that tend to reward investors over time. Career Builders have the power of time on their side. Investing early in your career is always a good idea.

In addition to the issue of market concentration, there are beginning signs of a cooling economy. We can’t say that a recession is around the corner. U.S. economic growth continues, inflation is crawling lower, and consumer spending on services (travel, etc.) is strong. However, unemployment claims are rising. Broad consumer spending and housing sales are both slowing. Disinflationary forces are beginning to be felt and the earnings growth needed to support stock prices could become challenged. We advise Established Professionals to keep safer investments for money needed in the shorter term. But it is important to keep a long-term perspective for your retirement savings. Fear of the short-term and the emotional investment responses it can cause can be a major detriment to meeting your goal.

In a market trading at 24x earnings, some healthy caution is in order, but we’re not reducing stock exposure at this point. Despite the market’s concentration risks, overall corporate earnings should strengthen the remainder of this year and beyond. Over long periods, markets trend higher, even with downturns and corrections along the way. Our portfolios are structured to withstand these downturns, with money needed in earlier retirement years invested most conservatively.

There is still the question of how long interest rates will remain elevated. We expect to see inflation moderate, and the Fed lowering interest rates as early as September. This should allow capital-intensive businesses and commercial real estate borrowers to refinance at lower rates – feeding economic activity and supporting those smaller-cap stocks that have underperformed the largest companies.

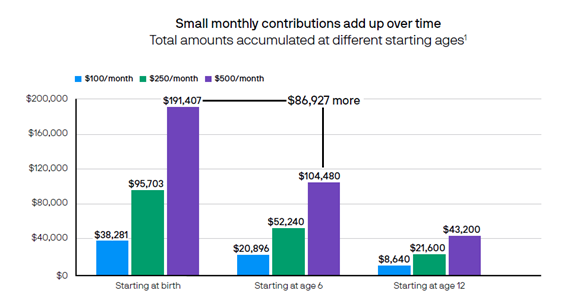

Many families list paying for a child’s college education as an important financial goal, yet are unsure how much to save. College tuition costs have increased much faster in recent decades than any other household expense. J.P. Morgan recently projected that a four-year college education for a child born today will cost between $250k and $580k (ranging from public in-state tuition to private tuition). At the same time, financial aid awards have declined.

If you’re the parent of a newborn, the need for college planning may seem far in the future. But starting early can make a huge difference, even if making small monthly contributions.

A tax-advantaged savings vehicle has the potential to grow faster, as taxes aren’t taking a bite out of your investment returns.

In honor of National 529 Day on May 29th, here we highlight some facts about 529 accounts as a tax-advantaged vehicle for saving and investing for college.

You may get an income-tax break on contributions made to a 529 offered by the state you live in.

Money saved in a 529 has the potential to grow tax-free. Earnings on the money contributed are not taxed while in the 529 account, and money can be withdrawn free from federal income tax if used for qualified educational expenses, including an amount for room and board, and even an annual amount for K-12 education.

Most states also don’t impose state income tax on qualified withdrawals.

Taking money out of a 529 for non-educational expenses triggers tax and penalty only on the gains.

The beneficiary of a 529 account can be changed at any time to another family member or even to yourself. And there is no limit on how long a 529 account can exist – theoretically allowing an account to be passed down generations.

Family and friends can make contributions to your child’s 529, and if a non-parent is the account owner, the money in the 529 plan does not impact federal financial aid.

Subject to certain limitations, up to $35,000 of unused money in a 529 account can be rolled over to a Roth IRA in the beneficiary’s name, without any taxes or penalties related to taking money out for non-educational expenses.

1 J.P. Morgan Asset Management. This hypothetical example illustrates the future values at age 18 of different regular monthly investments for different time periods. Chart also assumes an annual investment return of 6%, compounded monthly. Investment losses could affect the relative tax-deferred investing advantage.

Most 401(k) and other retirement plans offer Target Date Funds (TDFs) as a default choice. They have become increasingly popular for a few good reasons but are rarely the best solution once your accounts achieve some size.

Let’s look at how they work and whether they are the most efficient choice for you.

TDFs are a great choice for beginners, or when you join a new employer plan. There is usually a lineup of funds targeting retirement dates in increments of five or so years. The concept is that the fund becomes increasingly conservative as the target date approaches, but that is a one-size-fits-all approach that can’t take your unique needs into account.

So, when are TDFs not the best investment choice?

To start, all of your money is invested with one fund family, instead of getting different approaches and methodologies. These funds are also usually invested across all asset classes and industries instead of those best suited to the current economic environment. They also evenly spread bond exposure instead of actively selecting the most appropriate bond sectors.

The biggest challenge with TDFs is that you don’t want all your investments too conservative as you enter retirement.

Yes, you want to make sure that you have some conservative assets to draw from during rough patches, but you still need growth during retirement to keep pace with inflation.

Here are a few things to consider:

· Do you actively rebalance your accounts?

· Does your plan have tools to evaluate your allocation vs. your goals and timeframes?

· Do you compare what you own against what’s available?

· Have you considered the advantages of an IRA for funds in an old employer plan?

· Are you layering investment risks to match your goal timeframes?

Changes to the FAFSA form and the formula for determining a family’s need for aid are changing, effective for the 2024-2025 school year. While all the changes are beyond the scope of this post, here we highlight two from a financial planning perspective.

Parent Income:

Contributions (pre-tax salary deferrals) to employer retirement accounts are no longer added back to parent income. This could be an additional incentive for parents with employer plans to max out contributions in years that the FAFSA looks at income. The FAFSA looks at the year two years prior to the beginning of the school year. For example, the 2024-2025 school year looks at 2022 income. Note that this change only applies to contributions that come straight from a salary reduction. Contributions to IRAs that are deductible on the tax return are still added back to parent income.

Grandparent Contributions: Up until now, while grandparent (or other non-parent) owned 529 accounts did not count towards a parent or student’s assets, withdrawals from said account counted as income to the student which had to be reported on the FAFSA. This could reduce the student’s aid eligibility. With the changes, withdrawals from a third-party owned 529 account will no longer count as student income. Grandparents can now maintain a 529 account for their grandchildren and distribute funds without impacting aid eligibility.

Because of these changes, the 2024-2025 form will not be available until December this year. You can stay up to date on announcements at https://studentaid.gov/, or through college financial aid office websites.

Call us to review your investment approach (404) 941-2800.

Laser-focus on inflation was the key driver of both interest rates and market performance over the past two years.

Inflation continues retreating towards the targeted 2% range, which should largely be achieved around mid-year. We expect the Fed will begin lowering rates during the summer. While the bond market has priced-in 6 rate cuts for the year, beginning as early as March, we believe it will be a more modest and later cutting cycle. From there, the narrative should shift from inflation and interest rates back to the fundamentals of economic growth and earnings. There is still a risk that the economy could pick up steam and inflation return to haunt us once again, a la 1980. Nor are we out of the woods of potential economic weakness. But we see light at the end of the tunnel.

We remain optimistic about the long-awaited resurgence of small-cap, value, and international stocks closing the performance gap versus U.S. large-cap growth over the ensuing economic cycle.

The old maxim of ‘no tree grows to the sky’ will ultimately prevail. We find it unlikely that valuations of the “Magnificent 7” can continue to rise unabated. Valuation is a fundamental driver of long-term performance, and small caps and international markets remain undervalued relative to history.

As we expect a return to economic fundamentals over 2024, much depends on the economic growth and labor productivity needed for earnings to meet or exceed expectations. Should the economy slow, stock markets will have a hard time producing meaningful gains. While not our base case, we will remain mindful of the many economic indicators still flashing red.

We understand it is an election year. As November approaches, we typically see markets stagnate or slightly decline as the uncertainty and anticipation mounts. However, history tells us that regardless of who wins, there is negligible impact on financial markets in aggregate. In the end, regardless of whether your favored party wins or loses, there is no advantage in changing investment policy.

The normalization of interest rates is an uncertain path and forecasting economic growth is even more difficult. As investment themes change throughout the year, we will be looking for areas where valuation and earnings potential appear strongest – a disciplined approach that has served us well long-term.

What remains paramount is our desire to always take care of our clients’ current investment needs, while working towards achieving long-term investment goals.

With our time horizon investment process, we have successfully sheltered near-term spending needs from market disruptions, giving the longer-term assets the time needed to allow these disruptions to play out. Our long-held mantra of “go live life, we’ve got your back” has worked throughout this period of upheaval and we will be making sure that continues.

So, enjoy today and tomorrow, and let us do the worrying!