Today, U.S. stocks are relatively concentrated. An investor in the S&P 500 is putting 40% of their money in the 10 largest companies. Historically, such concentration doesn’t work out well. The S&P 500 is also expensive. Such a concentrated and expensive market requires corporate earnings to continue growing unabated (to support the prices).

There is rarely economic certainty but until new government policy and the resulting economic impacts are understood, you should expect fairly big market swings. It’s been an unusually long time without a market correction (a 10% decline). One or more market corrections this year would not be surprising, so you should be thoughtful about how your portfolio is invested.

Market corrections can come and go in short order. More protracted declines take longer to develop and recover from. It isn’t so much the loss of value that has the most impact on your portfolio, and your well-being. It is the loss of time. Value will rebuild itself. The question is, do the growth assets in your portfolio have that time?

Integras Partners’ Time Horizon Investment Process can help. You can sustain your lifestyle with the money we set aside in Income Strategies, which provides the time needed for our Growth Strategies to capture the growth rewarded by volatile markets. You’re always welcome to speak with us about how we might guide you. The greatest value we can provide clients is the ability to not worry about money, and to go live life!

Call us today to learn how we can help. 404-941-2800

You’re on your financial journey and we can help people pave their own path. This quarter’s commentary blogs start with a recap of 2024 and our views of economic conditions. Then we share some of our ideas for timely investing. You’re always welcome to speak with us about how we might guide you.

2024 was a year of Artificial Intelligence and the biggest company stocks. Despite December weakness, the S&P 500 Index (a common barometer of the U.S. stock market) gained 25% for the year. However, most of this gain was isolated in the largest and most growth-oriented stocks (most of which are heavy into AI), which investors paid more and more for. Smaller companies showed some strength but faltered as concerns about Inflation prospects and continued economic growth kept coming up. Still, small cap stocks finished the year up 11%. Our robust gains were not shared by the rest of the world. And bonds provided a mild 1.3% return.

Our economy is growing at a healthy rate with low unemployment and inflation around 3%. This supports continued corporate earnings growth and possibly the quite high stock prices we have today. The near future appears primed for further growth as many U.S. consumers are getting raises, have little debt, lots of credit available and job security, all of which encourages more spending. While this all sounds supportive of another good year for markets, you must also consider risks to this view, specifically the relatively high stock prices and how further economic growth impacts inflation and interest rates.

The more an economy grows, the more demand there is for money, which increases long-term interest rates. Also, some policy initiatives voiced by the new administration (i.e. tariffs and deportation) are likely to result in higher costs for US companies. Regulatory reform and a more relaxed tax regime should boost earnings growth. Over the last 3 months, long-term interest rates have risen at almost the fastest pace ever because of these possibilities, and they could potentially go higher. Higher interest rates put downward pressure on stock prices, especially when they are already high.

With stock dividends getting taxed twice (once to the corporation and again to the shareholder), many companies are now choosing to return profits to shareholders in the form of stock buybacks instead. While there are several other reasons, the primary one is this tax-efficiency. Many of these companies do not pay a cash dividend sufficient to be included in our dividend growth strategy today. Integras Partners has historically viewed cash dividends as a sign of corporate strength, but this year we are introducing a new metric to our screening processes that includes these companies in the pool of candidates for investment.

Contact us to learn more about our strategies and how they can help you get where you are going. Call us today to learn how we can help. 404-941-2800

As we age, living situations and health needs will change. Parents and their children avoid planning for them, for very understandable reasons:

Parents don’t “want to be a bother”. Kids “don’t want to pry” into their parents’ lives. Money conversations can be tense. Parents don’t want to choose one child over another to take important roles in making health and financial decisions.

Our Generational ConversationsTM program helps adult children and their elder parents navigate planning for Housing, Care Management, Financial Continuity, Legal Strategies, and Security.

We want to help. As families get together over the holidays, it’s a great time to broach these subjects. Click here to download our free Themes for Family Conversations. We wish you all the joys of the holidays and everyone in your family a little extra peace.

Call us today to learn how we can help. 404-941-2800

Working with Integras Partners brings confidence to your financial journey. We help clients not worry so much about money, knowing that an expert is minding your investments.

Many individual investors let emotions and procrastination impact their decisions – hesitating to buy when prices fall and feeling eager to invest when markets are strong. A disciplined advisor provides steady, informed guidance to improve your financial outcomes.

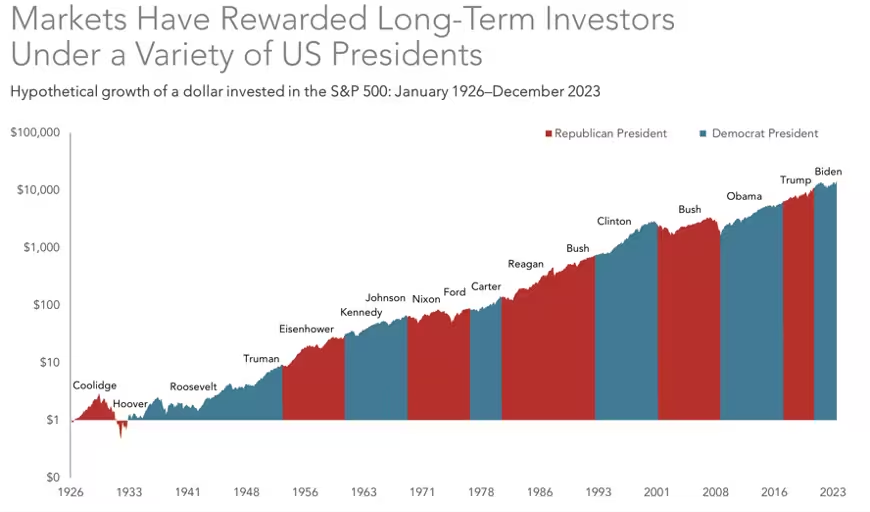

Elections can stir strong emotions, but don’t let them delay your investing. Historically, markets are influenced more by economic fundamentals than politics.

Stock values fluctuate under every president, but the S&P 500 Index® trends higher over the long term, no matter who’s in the Oval Office.

Source: Dimensional Fund Advisors

Or which party controls Congress:

Source: Dimensional Fund Advisors

Market reactions to elections create short-term volatility, but defensive changes to your investments are usually detrimental. Regardless of tax policy or regulations, factors like corporate earnings growth, economic conditions, and technological advancements have more impact on market performance.

Integras Partners with clients to keep a long-term perspective, overcome emotional delays, and take action. By keeping short-term cash needs invested with less market risk, we give clients the peace of mind to keep longer-term money invested and feel more comfortable during periods of short-term market craziness.

August through October are historically the weakest and most volatile period for stocks and bonds alike. This year appears to be exceptional. Few expected the strength and resilience demonstrated by financial markets in the third quarter. The S&P 500 Index® posted a stellar 5.77% gain, posting year-to-date gains of 22%. Unlike recent years, the gain was not due to only a few large tech and communications stocks. We’re seeing overdue and much preferable broadening of stocks showing positive returns, and not just from the largest U.S. companies, but in small-caps and foreign markets as well.

The economy remains strong as the Fed begins its interest rate cutting cycle. Not too hot, and not too cold. Just like the story of a lost girl, everything is now “just right”. The Fed is done raising rates, employment strength continues, and economic growth is solid. These conditions amount to a “Goldilocks Scenario”, just about perfect to sustain corporate earnings growth and stock gains. Earnings growth should accrue to the value and small cap sectors, which until recently have lagged the large tech-dominated themes that were driving the market. At Integras Partners, we have been increasing our client allocations to these undervalued areas of the market for several months.

With lower relative prices, small-caps in particular should become even more attractive to investors, given that this Goldilocks scenario lasts for a while. We saw some confirmation of this in the third quarter as the lower P/E stocks began to outperform.

Integras Partners makes it easier to stay invested by actively managing client portfolios across our time-horizon strategies. We do this by keeping low-risk investments to provide for near term goals, allowing you more comfort with keeping longer-term investments intact through market swings. We can help you capture the long-term gains that volatile markets generate over time with less stress.

First, you may want to read our current market commentary. It details why the markets are particularly attractive right now. You can check it out here.

Employer retirement plans are often your greatest investment, for several reasons.

Funds tend to stay invested long-term, riding out down cycles to capture real growth

Salary-deferral investments made with every paycheck take advantage of market moves buying more shares when markets are down, and less when prices are higher.

Many employers match some contributions to help build your retirement funding.

Don’t limit your contributions to only capture your employer’s match.

Remember that Traditional 401(k) deferrals are pre-tax, so an extra $100 a month typically reduces your bi-weekly paycheck by only $32.

The 2025 contribution limit is $23,500. If you’re 50 or older, you can add another $7,500.

Do you still have money in a former employer’s plan?

Employers have greatly narrowed plan investment choices to avoid liability after the tech bubble of 2001.

Some plans restrict investment choices to “target date” and generic index funds.

If you’re retirement-minded, you can “rollover” an old 401(k)’s balance to an IRA without tax impact, usually getting greater freedoms in how you invest and spend your savings, including your own tax withholding choices.

Glen & Amber are sandwiched between their elder parents and three children, ages 15-24. Glen has been managing their investments on his own and would like to retire from his corporate job. With family pressures complicating this decision, friends referred them to us for financial advice.

In our Discovery Meeting, we learned that Glen’s parents are in their late seventies and becoming less independent. His sister lives closest to them but increasingly frequent trips are straining her family. Amber’s parents are divorced; her dad and his wife are stable, but her mom is struggling with health and financial issues.

Seeking comfort for Glen’s career decision, we started with the family needs. Through our Generational Conversations program, we provided comprehensive information on care management options. Hiring occasional home caregivers who report to Glen’s sister proved to be a good solution. Amber’s mother moved into independent senior living at a reasonable monthly cost. She is now happier in a social setting and Amber is greatly relieved. The proceeds from selling her mom’s home combined with Social Security will keep mom financially stable for many years.

The couple’s elder daughter, Olivia graduated college with some 529 funds remaining, which we transferred to their middle child. Olivia is now largely independent with a first job, and gets occasional support from her parents.

In addition to increasing 529 contributions for the younger kids, we opened custodial (or UTMA) accounts. These are irrevocable gifts that a parent controls until the children reach their state’s age of majority. Unlike 529’s, they can receive annual gifts of stock and mutual funds and get a preferential tax rate on sales. Glen gifted some appreciated company stock which was promptly sold. The proceeds can immediately cover some extracurricular expenses and later fund college costs ineligible for 529’s like cars, Greek life and entertainment.

With family issues addressed, we narrowed in on the retirement conversation. We explored Social Security strategies. Glen also expects some consulting opportunities. We all agreed to start managing Glen and Amber’s investments right away. Our paradigm of aligning investments to match expected income needs brings comfort around retirement spending, while capturing growth with longer-term dollars.

Generational Conversations also supports adult children and their elder parents to plan for housing, legal strategies and security needs.

First, let’s look at the three types of accounts by their tax treatment.

Tax-Deferred Retirement Accounts are funded with untaxed dollars (contributions are tax deductible, either through salary-deferral or on your tax return). However, future withdrawals are fully taxed as ordinary income. Examples include 401(k)s and traditional IRAs.

Taxable Accounts are funded with after-tax dollars. Dividends and gains from sales receive preferential tax rates. Because you’re paying taxes in the years that income or sales occur, withdrawals aren’t taxed. These are usually mutual fund and stock accounts.

Roth Account contributions are not tax deductible. However, they grow tax-free forever, and withdrawals are never taxed.

It’s best to spread money across these three account types while you are working. This will give you some flexibility to manage your taxes in retirement, which could help your money last longer. Having different types of accounts also provides options for early retirees.

Optimal investment and withdrawal strategies are different for everyone. Factors include age, tax brackets, employer plan features, and investable income. Powerful retirement planning is best done well in advance and then annually while taking distributions.

Retirement planning is one of the most important things that we do for clients. We would be happy to discuss your situation and how we might be of service.