Meet Megan. She’s in her early 30s, single, and fairly stable in her career, although she may change employers.

Like most younger professionals we work with, Megan was unsure how to get started. She had a couple of previous company retirement accounts and a Roth IRA she started years ago. She had accumulated a sizable bank account but was unsure how to invest, especially after seeing her parents experience mixed results.

Integras Analysis

Our conversations determined that she was living within her means, but she needed a cash safety net (for unexpected events such as car repairs or job loss). She hopes one day to start a family and own a home. She contributes to her 401(k) but was unsure if she was contributing enough.

Recommendations

Put some of the excess cash in her bank account into a high-yield savings account for emergency / unexpected expenses

Allocate her remaining excess cash into two strategic accounts. First, a moderate account seeking 4% to 5% returns for goals in the next 3-5 years, such as purchasing a home. Then, a growth account seeking appreciation for longer-term goals before retirement age.

A modest increase to her 401(k), to better pave the path to future retirement. A 2% increase for someone earning $100K typically only lowers bi-weekly take-home pay by about $50.

Open a Roth IRA

Consolidate her former company plans to ensure she’s not losing track of these investments.

Results

With her “safety net” in place, Megan started an automatic bank draft of $100/month to her moderate account and is comfortable making monthly contributions to the Roth IRA. Besides tax-free growth, once you’ve owned a Roth for five years you can withdraw up to $10,000 without penalty towards a first-time home purchase! We consolidated her former company plans and helped allocate her current employer’s 401(k). Now, Megan’s retirement investments complement each other, and she has a track to meet her future retirement goal.

Inflation is one of the major risks to retirement. We’re all living longer, and the things we spend more of our money on in our older years (healthcare, senior housing) have the biggest price increases.

The recent inflationary environment is fresh in everyone’s mind, but even 2% inflation (the Fed’s current goal) is a risk to a retiree’s spending power over time. In a simple example, a $100,000 lifestyle when you initially retire would cost you over $148,000 in 20 years, assuming prices rose at a constant rate of 2%.

Inflation can’t be controlled, but evaluating it within your retirement plan can help identify ways to mitigate it. Here are a few ways inflation can be considered.

Investment Allocation: Investing too conservatively may mean that your investments won’t meet your spending needs long term. You want to make sure that you have enough invested for growth to keep up with inflation. This is not a static allocation. Integras Partners’ investment strategies are designed to align with anticipated inflation-adjusted spending needs over time.

Investment Selection: Investment selection within your portfolio is also a consideration. For example, there are types of investments that typically keep ahead of inflation, such as companies with a history of dividend growth and real estate.

Social Security Claiming Strategies: Delaying social security can give you higher lifetime benefits, but factors such as health and longevity must also be considered.

Strategies to Offset Healthcare Costs: Healthcare costs can be significant at older ages, and costs inflate at higher rates than other spending categories. Evaluate long-term care insurance or how to best make use of an HSA.

Withdrawal Strategies: Withdrawing too much in early retirement years, or having to sell assets to meet withdrawals during down markets are major risks to the longevity of a portfolio. Dedicate a portion of investments to near-term spending needs using relatively conservative, liquid investments. Drawing from that portion of the portfolio allows longer-term assets to remain invested for growth (to keep up with inflation), with the time needed to recover from market downturns.

Clients often ask us how to begin investing for their kids or grandkids. As always, starting early pays the greatest benefits. Here are two ideas to consider:

529 Plans allow you to invest cash for school expenses. The 529 account grows tax free, and money taken out for qualified education expenses is not taxed. These accounts are typically owned by a single parent, with one beneficiary. They are state-specific and can accept high contributions.

Almost all states offer income tax deductions for contributions to their state 529 plans. Some states offer tax breaks for investing in any state’s 529 plan.

Not all plans are created equal, with investment choices limited to that plan’s fund lineup. Most plans offer target-date funds which are a good idea to align with HS graduation.

The definition of qualified education expense has broadened over the years. Beginning in 2026, $20k in annual distributions are allowed for K-12. Other qualifying expenses include college apps, housing, and even exam-prep and computers.

Beneficiaries can be changed to other family members.

Once a 529 account has been open for 15 years, unused funds up to $35K can be rolled into a Roth IRA for the beneficiary (subject to annual Roth eligibility and contribution limits).

UTMA (Custodial) Accounts are irrevocable gifts to a minor. These accounts can accept not only cash, but gifted securities as well. Minors have very low tax brackets which enable some gains to be realized tax free, or at a very low rate.

Funds can be used for almost anything for the benefit of the child, including cars, extracurricular activities, travel and Greek life.

This can be a great tool for gifting appreciated stocks or mutual funds, selling with minimal taxes and using the proceeds to cover those athletic or extra-curricular activities.

Grandparents and others can directly gift to these accounts!

UTMAs are considered assets of the child and can decrease financial aid eligibility.

Parents often pair a 529 plan with a UTMA, to take advantage of the features and uses of both.

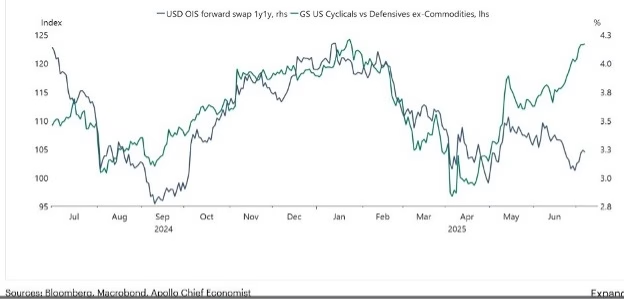

The Fed remains reluctant to lower short-term interest rates, as the inflation outlook heads back up towards 3%. Slowing economic growth and sustained employment weakness would prompt rate cuts.

The technical chart below reflects that the bond market is expecting slower economic growth. Projections are for two interest rate cuts before the end of the year.

Equity markets are signaling the opposite, by valuing cyclical stocks higher than defensive stocks. This happens when the broad market expects an acceleration of economic growth (which leads to higher rates).

Both cannot be right. Either the bond market is wrong and interest rates will move higher, or the stock market is wrong and will see declines. No one knows which it will be. This is the dilemma investors face when positioning their portfolios.

At Integras Partners, we recently increased our more defensive allocations. Markets are shrugging off multiple concerning trends. There are downside risks in a cautious U.S. consumer, slowing economic growth, and weaker employment data not yet reflected in market valuations.

We have concentrated our growth allocations in those sectors less likely to be negatively impacted – sectors where strong secular growth trends remain in place.

It is our nature to err on the side of caution. Chasing returns is not our primary objective. We are motivated every day to ensure that our clients are positioned to enjoy their lifestyle, without worrying about what’s going on short-term in the markets.

If this approach sounds like a good fit for you, please reach out to learn how we can help!

There is an old Wall Street saying that ‘the market goes down in an elevator and rises on an escalator’. The market did indeed fall like an elevator in March but then took the elevator right back up. As tariff postponements soothed markets, stocks staged a major relief rally that continues as of this writing. Simultaneously, the superiority race over artificial intelligence, onshoring production of essential products and increasing operational efficiencies continues unabated across virtually all industries.

After a 19.5% decline which extended through the first week of April, the S&P 500 Index® rebounded a surprising 9.8% during the remainder of the 2nd quarter. The best performance was garnered overseas as the MSCI EAFE Index® finished the quarter up 10.7% and is up 20% YTD. We were glad to see markets finally recognize the cheaper and stronger dividend-paying foreign companies, which we think will continue near-term.

While the détente in the most punitive tariffs sparked the April recovery, the prospect of tariffs has not disappeared. They negatively impact corporate earnings, employment, and inflation. Some companies’ stocks have already been squeezed. The market response to these companies’ quarterly reports will be an interesting indicator of what may manifest later this year.

Future earnings are what matter when valuing a company.

Tariffs will likely remain in place to some degree across most industries, so how companies handle increased costs will sway stock prices.

Economic growth is slowing slightly, and we will closely monitor U.S. consumer strength as data is released over the next months. Anecdotal evidence implies that consumer spending remains strong but is beginning to slow. Employment remains firm as businesses are retaining employees but not hiring many new ones. Strong employment kept us from recession a couple of years ago as consumers had the confidence to continue spending. We don’t expect a major shift, but with today’s elevated stock prices any consumer weakness could cool investor optimism. Unless companies can show earnings growth in a slowing economy, markets will decline. Sectors and industries making major capital expenditures aimed at artificial intelligence and supply chain realignment should be fine, but for others, it will be a challenge.